By Dawood Jarral, CFA, Market Policy Analyst | Global Economy

(PM Youth Loan) At-a-Glance Summary (Key Takeaways)

| Feature | Detail |

| Status | New 2025 application batch officially open |

| Maximum Loan | Up to PKR 7.5 Million |

| Tier I Benefit | 0% Mark-up (Interest-Free) up to PKR 500,000 |

| Application Method | 100% Online via Digital Youth Hub |

| Urgency Level | High – Limited funding cycles |

| Recommended Action | Apply immediately to secure priority processing |

The Opportunity: Zero-Interest Loans Are Back for 2025

The opportunity Pakistani youth entrepreneurs have been waiting for is officially live. Following a period of restructuring and policy refinement, the government has reopened applications for the Prime Minister’s Youth Business & Agriculture Loan Scheme (PMYB&ALS) 2025 — a strategic financial initiative designed to empower new and existing SMEs with affordable capital.

This is not merely a routine program continuation. The 2025 batch reflects a focus on transparency, streamlined processing, and targeted economic impact. Eligible applicants can now secure up to PKR 7.5 million, including interest-free funding under Tier I, making this one of the most impactful financial tools for youth-led entrepreneurship in Pakistan.

As a Market Policy Analyst, I have reviewed the updated guidelines in coordination with partner banking institutions. The system is live, funding is cycle-based, and early applicants carry a measurable advantage, particularly for the highly competitive Tier I (0% mark-up) loans.

What’s New in the 2025 Batch?

The latest PMYB&ALS iteration introduces reinforced digitization through the Digital Youth Hub, now the sole application channel. This change is intended to:

- Increase transparency and accountability

- Reduce processing delays

- Prevent unauthorized intermediaries

- Enhance real-time monitoring by partner banks

Applicants must ensure that their CNIC is valid and NADRA-verified before initiating the application. Incorrect or expired details will result in automatic rejection.

Are You Eligible? Mandatory Requirements

To avoid instant disqualification, applicants must meet the following conditions:

Age, Citizenship & Business Eligibility

- Pakistani citizen with a valid CNIC

- Age between 21–45 years

- IT/E-commerce applicants: Eligible from age 18 with matric or technical certification

- Business falls under SME category (startup or existing)

Who Is Not Eligible

- Government employees (Federal / Provincial / Semi-Government)

- Individuals with prior loan defaults

- Applicants submitting multiple parallel applications

Funding Structure: Tier-by-Tier Breakdown

| Tier | Loan Amount | Mark-up Rate | Security | Repayment Tenure |

| Tier I | Up to PKR 500,000 | 0% | Personal Guarantee | Up to 3 Years |

| Tier II | Up to PKR 1.5 Million | 5% | Personal Guarantee | Up to 8 Years |

| Tier III | Up to PKR 7.5 Million | 7% | As Per Bank Policy | Up to 8 Years |

Why Tier I is Most Competitive

Tier I is fully subsidized by the government, making it interest-free. It serves micro-entrepreneurs and startups needing working capital or essential equipment. Due to limited allocations, approval is highly competitive.

Tiers II and III support business expansion and scaling, suitable for structured SMEs with collateral readiness and strong financial forecasting.

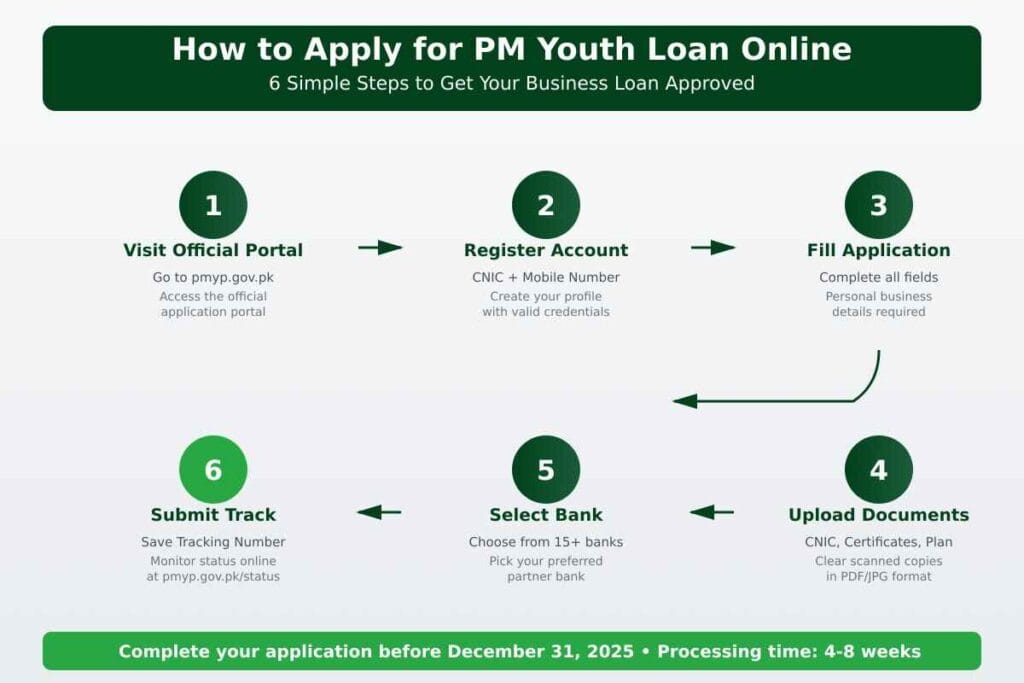

Step-by-Step: How to Apply Online (PM Youth Loan)

Phase 1: Preparation

- Verify CNIC validity

- Prepare digital documents:

- CNIC copies

- Utility bill

- Academic certificates

- Business plan (mandatory for T2 & T3)

- Keep PKR 100 processing fee ready

Phase 2: Digital Youth Hub Application

- Access official Digital Youth Hub

- Click “Apply Now”

- Complete personal & business information

- Select partner bank

- Upload documents

- Submit & save Application ID

You will receive an SMS confirmation upon successful submission.

How to Check Application Status

- Visit Digital Youth Hub portal

- Navigate to status tracking

- Enter CNIC and Application ID

- Review status: Submitted / Under Review / Approved / Rejected

Common Mistakes That Lead to Rejection

- Poorly written business plans

- Mismatched CNIC details

- Applying for Tier beyond eligibility

- Missing documents

- Selecting unsuitable banks

Expert Tip: A well-structured business proposal with revenue forecasts improves approval chances significantly for Tier II & III.

Important Timeline & Funding Reality

- 2025 cycle funds are release-based

- Applications are processed in waves

- Early submissions receive faster approvals

- Delayed applications risk fund exhaustion

Recommendation: Apply immediately to secure position in the current cycle.

Official Helpline & Support

- National Youth Helpline: 0800-69457

- All technical support available via Digital Youth Hub

Always verify information through authorized government channels only.

Trust & Source Verification

Content verified through:

- State Bank of Pakistan SME Guidelines

- Digital Youth Hub official documentation

- PMYB&ALS partner banks policy updates

Conclusion: Act Now — Secure Your Financial Future

The PM Youth Loan Scheme 2025 represents an unprecedented opportunity for Pakistan’s youth to convert entrepreneurial ambition into sustainable enterprise. With zero-interest funding available and a fully digitized process in place, the path to business ownership has never been more accessible — or more competitive.

Delaying your application may cost you access to critical capital. Act decisively. Prepare thoroughly. Apply immediately.

Have you started your application? Share your experience or questions in the comments below.

How do I apply for the PM Youth Loan 2025 online?

Apply 100% online via the Digital Youth Hub (PMYP) portal — go to the PMYB&ALS section, click Apply Now, fill the form, upload documents and submit. You’ll receive an application ID by SMS.

Who is eligible for the PM Youth Loan?

Pakistani citizens with a valid CNIC; age 21–45 (for IT/e-commerce applicants the lower limit is 18 with at least matric/technical certification). Some exclusions (e.g., government employees, prior defaulters) apply.

What are the loan tiers and interest/markup rates?

Tier I: Up to PKR 500,000 — 0% mark-up (interest-free)

Tier II: Up to PKR 1.5M — ~5% mark-up

Tier III: Up to PKR 7.5M — ~7% mark-up (collateral/specific bank policy may apply).

What is the maximum loan amount under the 2025 batch?

Up to PKR 7.5 million (Tier III).

What documents do I need to apply?

Typical documents: CNIC, recent utility bill (address proof), passport-size photo, educational certificates, business plan (mandatory for Tier II/III), and any collateral/guarantor docs if requested. Always upload clear, readable scans.

Is there an application fee — and how much?

Yes — a non-refundable processing fee (includes NADRA verification) is charged. The official guidance lists PKR 100 as the processing fee.

How can I check my PM Youth Loan application status?

Use the Digital Youth Hub’s Track Application / Status page: enter your CNIC and the Application ID (sent by SMS) to see statuses like Submitted, Under Review, Approved or Rejected.

How long does approval and disbursement usually take?

Timelines vary by bank and funding cycle — expect verification & processing to take several weeks; early applicants in each funding wave tend to get faster approvals. (Apply ASAP to avoid fund exhaustion.)

Do women or special groups get reserved quotas?

Yes — the program typically reserves quotas (for example, for women entrepreneurs and other priority groups). Check the portal or partner-bank pages for current quota details by province.

What common mistakes cause rejection — and how do I avoid them?

Top rejection causes: mismatched/expired CNIC data (NADRA mismatch), incomplete or low-quality documents, weak business plans for Tier II/III, applying for an ineligible tier, or submitting multiple parallel applications. Fixes: verify CNIC on NADRA, scan documents clearly, craft a concise financial forecast, and apply only once.

𝑻𝒉𝒆 𝑷𝒖𝒍𝒔𝒆 𝒐𝒇 𝑮𝒍𝒐𝒃𝒂𝒍 𝑨𝒇𝒇𝒂𝒊𝒓𝒔